A Simple Guide for the Average Person

Why This Is So Confusing

Pre-tax. Post-tax. 401(k). Roth. IRA. HSA. The government’s alphabet soup of accounts doesn’t exactly scream simple. For the average person, the question is: Where do I actually put my money first?

Here’s the straightforward order, boiled down into plain English.

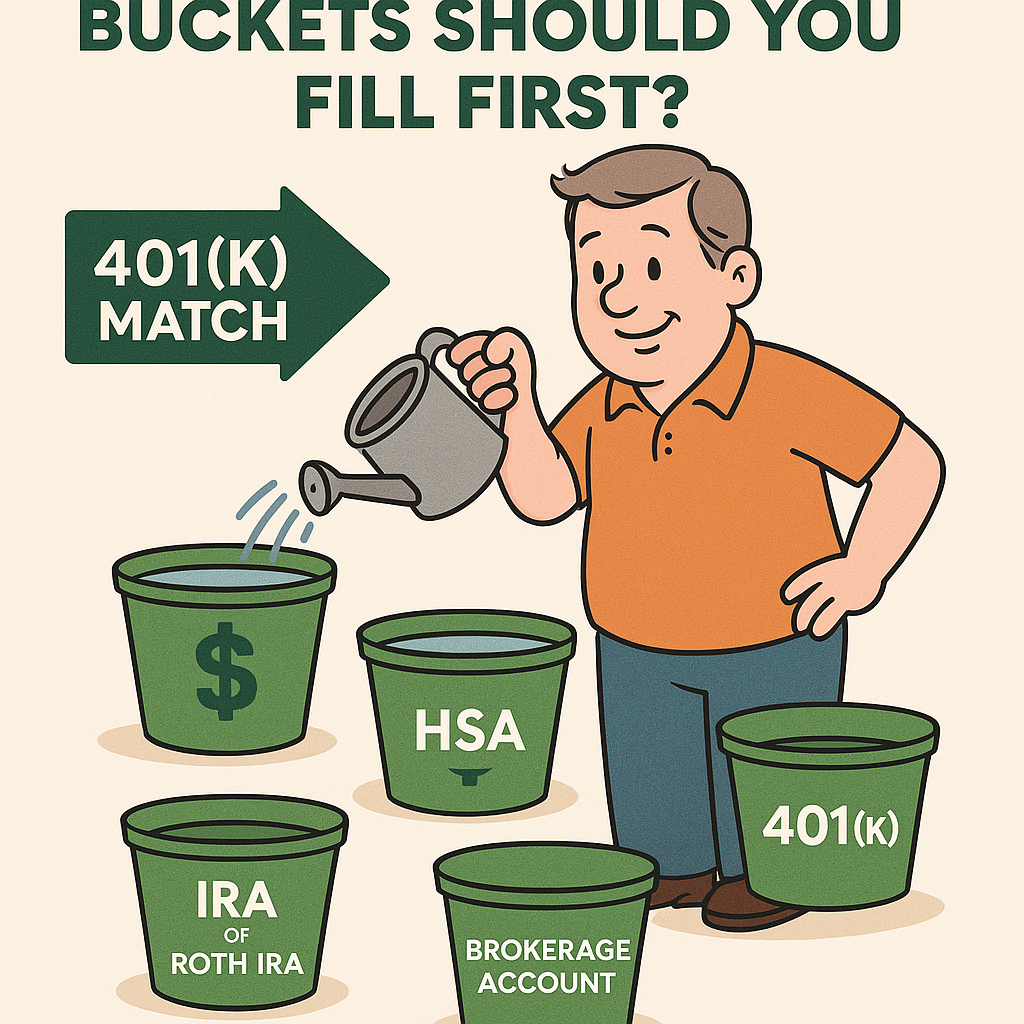

Step 1: Grab Any Free Money First

- If your employer offers a 401(k) or 403(b) match, contribute at least enough to get the full match.

- Why: It’s the closest thing to “free money” you’ll ever see in finance.

Step 2: Fund Your HSA (If Eligible)

- HSAs are the unicorn: tax deduction in, tax-free growth, tax-free out (for medical).

- If you can afford to pay health costs out of pocket and invest the HSA, it doubles as a stealth retirement account.

Step 3: Max Out Your IRA or Roth IRA

- Roth IRA: Great if you expect taxes to be higher later — tax-free growth and withdrawals.

- Traditional IRA: Deductible now, taxed later. Useful if you want the tax break today.

- Contribution limits are lower, but fees and investment choices are usually better than workplace plans.

Step 4: Go Back to Your 401(k)/403(b)

- Once you’ve hit the IRA cap, pump more into your workplace plan.

- Even without a match, the tax savings + higher contribution limits ($23,000 in 2025, plus catch-ups if 50+) make it worth filling.

Step 5: Use a Taxable Brokerage Account

- When you’ve maxed the tax shelters, keep saving in a regular brokerage.

- No tax perks, but total flexibility: no age restrictions, no penalties, no contribution caps.

- Perfect for goals before 59½, like early retirement, house projects, or bridging the gap.

The “Easy Button” Order of Operations

- Match in 401(k)/403(b) (if offered)

- HSA (if eligible)

- IRA or Roth IRA

- Back to 401(k)/403(b)

- Brokerage account

The Bottom Line

Don’t overthink it — the real power is consistency, not perfection. If you fill the buckets in this order, you’ll be ahead of 90% of people trying to decode the IRS puzzle.

👉 Related Reading: